More Drivers Owe More Than Cars Are Worth

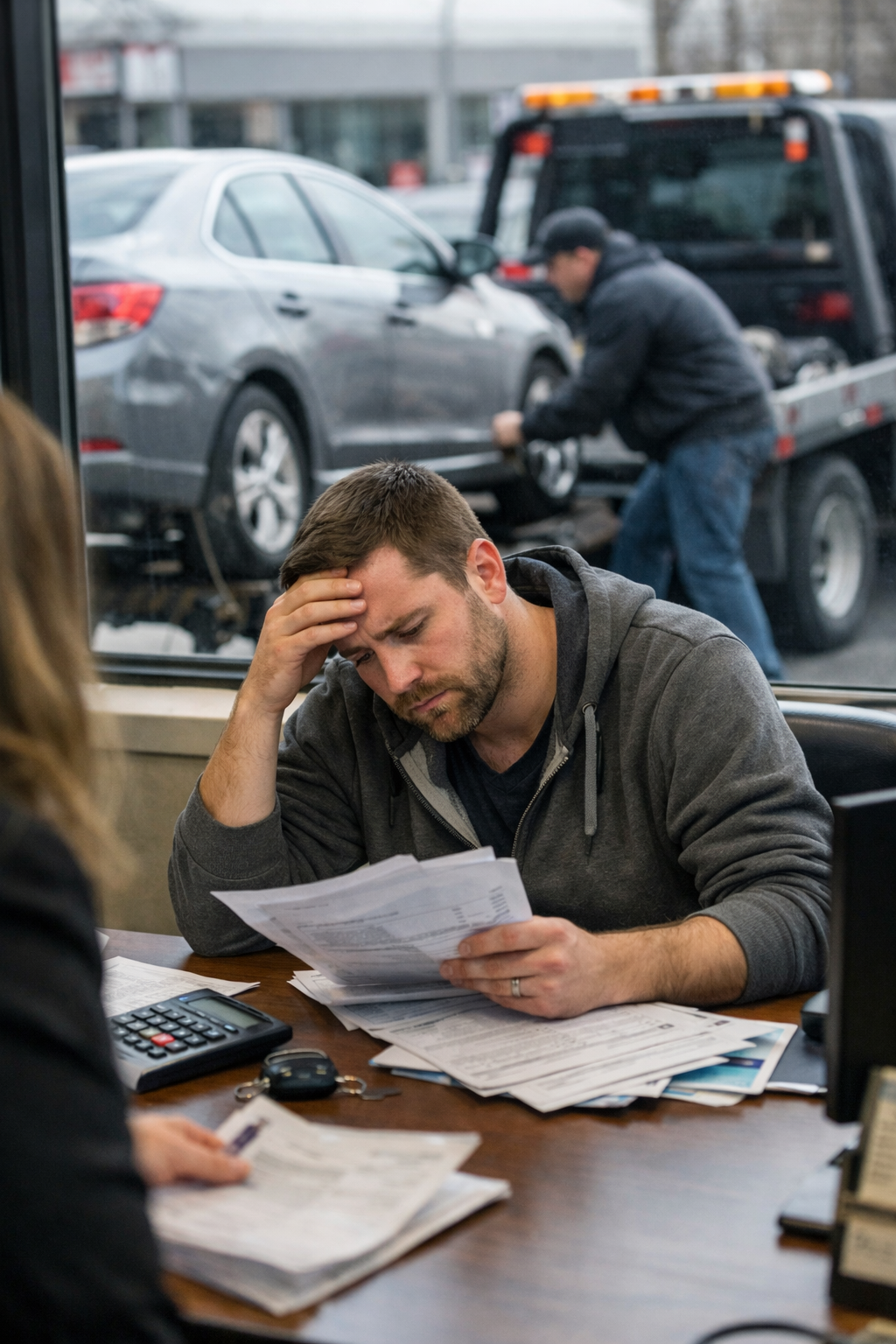

Rising numbers of U.S. car owners are finding themselves owing more on their auto loans than their vehicles are worth, a trend that underscores mounting financial strain among consumers and growing risks in the auto lending market.

According to the Wall Street Journal article titled “More Car Owners Are Upside Down on Their Auto Loans,” the share of borrowers with negative equity has been climbing as vehicle prices surged during the pandemic and borrowing costs increased sharply in its aftermath. Many buyers who paid elevated prices for new or used cars in recent years are now confronting the reality that their vehicles have depreciated faster than their loan balances.

Negative equity, often referred to as being “upside down,” can complicate efforts to trade in or sell a vehicle. Consumers in this position must either roll their existing debt into a new loan or cover the difference out of pocket, both of which can deepen financial vulnerability. The Wall Street Journal reports that some borrowers are carrying thousands of dollars in negative equity into new car purchases, contributing to larger loan sizes and longer repayment terms.

The trend reflects a confluence of factors that reshaped the auto market during and after the pandemic. Supply chain disruptions drove up vehicle prices, while low interest rates initially made financing more accessible. As inflation surged, the Federal Reserve raised rates, pushing borrowing costs higher just as used-car prices began to fall from their peaks. This combination has left many recent buyers exposed.

Lenders and dealers have continued to facilitate transactions by extending loan durations and increasing loan amounts, practices that can mask affordability issues in the short term but may increase risk over time. Longer-term loans, sometimes stretching to seven years or more, slow the pace at which borrowers build equity, prolonging the period during which they may remain underwater.

The situation poses broader implications for household finances and the auto industry. Higher monthly payments and persistent debt burdens can constrain consumer spending, while lenders face elevated default risks if economic conditions weaken. Although delinquency rates remain relatively contained, analysts cited by the Wall Street Journal note that stress is building, particularly among subprime borrowers.

For consumers, the shift serves as a reminder of the volatility inherent in vehicle values and the importance of loan structure. As prices normalize and interest rates remain elevated, the gap between what cars are worth and what borrowers owe may continue to shape the auto market in the months ahead.